Let me begin with thanks. Thank you all for being here, the Schumacher Center for hosting this gathering, and Peter Barnes for establishing the Common Wealth Prize and for all the work he has done over the years to lift up the radical idea of common wealth.

E.F. Schumacher’s Small is Beautiful presents a wide-ranging critique of large-scale property. What Schumacher had in mind was not only large-scale private ownership but also “over-centralized” state ownership. Quoting the famous historian R.H. Tawney, he recommended as an alternative to both “the decentralized ownership of public property.”

Building on this insight, I want to ask today whether big can be beautiful too. Not big and centralized, but big and decentralized. Is it possible to conceive of types of property that require the organization of society at large and the collective effort of all of us to bring them about? Could this also help to enable the kinds of human growth and richness of life that Schumacher thought possible?

Nature and the Economy

First, I want to say a few words about the environment, and how it is conceptualized in economics (or not). When I was a college student, economics and the environment were largely disconnected. In the early 1980s, when I went to graduate school at Oxford, there wasn’t a single course in environmental economics on the curriculum. Not one. And that really wasn’t all that long ago.

The economy was conventionally depicted as reciprocal interactions between households and firms. You can still find this pictured in every introductory economics textbook. There’s a circular flow in which the firms provide goods and services to households and receive dollars in exchange, and households provide labor and capital to the firms and get dollars in return. And this circle, it is supposed, merrily spins around like Earth on its axis.

What is oddly missing from this picture is the role of the natural world as both a source of raw materials and a sink for wastes from our production and consumption activities. Once we think about these functions of nature, we realize that even though they are often treated as free and unlimited, in fact they are finite. The source and sink capacities of nature available to us are limited, and if we fail to respect these limits we will run into serious economic and environmental problems.

Some of you will have heard this idea expressed in the phrase “limits to growth.” That is perhaps not the best way to put it. People often think of growth as good and closely linked to the fulfillment of human potential. A better way to put it would be to say that there are limits on how much we can use nature’s essential services.

The problem with ignoring the source and sink functions of nature is also sometimes described, again rather clumsily, as the “tragedy of the commons.” A better name for this is the tragedy of open access or, more precisely, the twin tragedies of open access, because the pitfalls are two-fold.

The customary “tragedy of the commons” parable starts with the example of commonly-owned grazing land. Everybody in the community can graze their cattle there, reaping the full benefit while not paying the cost to others of depleting the forage. The tragic result is that too many cattle are put on the land, degrading the commons to the detriment of all. We can imagine similar problems if we think about, for example, what city streets would be like if anyone could park wherever they wanted at no cost and with no rules as to where and when. We see the same problem in the pollution of air and water.

Calling these tragedies of “the commons” is a misnomer, however, because common property like grazing lands and forests are often very well-managed by communities that govern its use. The failure to recognize this has led to ill-conceived state interventions that end up spurring environmental degradation, the history of forest policy in India during British rule being a good example.

What really causes the tragedy of overuse is the absence of any kind of structure of rights and duties regarding access to the resource and its use. A better term for this situation is “open access,” meaning the total absence of any kind of property rights – private, public, or common.

There is a second tragedy that comes with open access as well. Although often neglected, I would suggest that it is no less significant. In the absence of well-defined rights over resources, they tend to be captured by people with disproportionate wealth and power—to the detriment of everyone else. This is the inequality side of the open-access problem. Proudhon once declared that “property is theft.” Sometimes this is true, but he was only half right: lack of property can be theft too.

The Price Conundrum

Thinking about the consequences of the failure to value the source and sink functions of nature, we come to what I call the price conundrum. In the wake of the recent presidential election that returned Donald Trump to power, many analysts blamed public concerns about prices and inflation. Polls revealed that high prices were the number one issue for a substantial fraction of those who voted for Trump. Prices are very visible, and most people are very tuned into them.

But there is a second problem with prices. Some things that appear to be cheap in the marketplace are expensive in ways not reflected in their price tag. The phrase “cheap is expensive” is the theme of a book by Raj Patel and Jason Moore called A History of the World in Seven Cheap Things. If we think about fossil fuels, for example, we can start to get a sense of the ways in which all the costs often are not reflected in market prices. When this happens, these misleadingly cheap things like oil will be used too much.

So, we’ve got a big problem: people are very worried about increases in the price of gasoline, or eggs, or other commodities, while at the same time some prices are in an important sense too low. Their market price does not signal the true costs involved in their production and consumption. How can we deal with this conundrum? How can we adjust prices to more accurately value true costs, while safeguarding family purchasing power?

One way to do this would be to raise people’s incomes enough to afford the increased prices. But here we come to another aspect of the conundrum. There is a mathematical symmetry between incomes and prices. Real income, a well-known concept in economics, is defined as nominal income adjusted for inflation. If incomes go up exactly as much as prices, real income is unchanged. Prices and income are both highly visible. People know the prices they face, and they know their incomes. So, on some level you may think, okay, we can raise prices as long as we raise incomes too. Things are good.

But there is a political asymmetry despite the mathematical symmetry. Most people think of prices as something beyond their control. Prices are something done to them. When they go to the gas station or grocery store and see a higher price tag, they think, “Ah, they’re doing it to me.” It may be the corporations doing it, or it may be the government, but somebody else is responsible.

In the case of income, feelings are different. Incomes seem to be the result of our own efforts. If income goes up, we tend to take the credit for it. The government may have good economic policies that encourage job growth and rising wages, but many of those who benefit think it’s really their own efforts that account for their higher incomes. Income is not something done to them, it’s done by them.

So we are back to the question: how do we correct prices that are too low without provoking a political backlash that torpedoes the policy? One possibility, in principle, would be to introduce a universal basic income along with the higher prices. Universal basic income would be highly visible, too, but would be equal for all. No one gets it because of their exceptional merit—everyone gets the same amount. This could perhaps make it politically feasible to allow prices that are too low to be raised.

But here we bump into another conundrum: how are we to pay for universal basic income? Where will we get the money? That’s always the stumbling block this the idea comes up against.

The Path to Net Zero

Let me turn now to the climate. The destabilization of our climate illustrates the dual tragedies of open access—the abuse of nature and the enrichment of powerful and wealthy people at the expense of everyone else—on a planetary scale. The limited capacity of the biosphere to serve as a sink for greenhouse gas emissions has long been mistreated as an open-access resource.

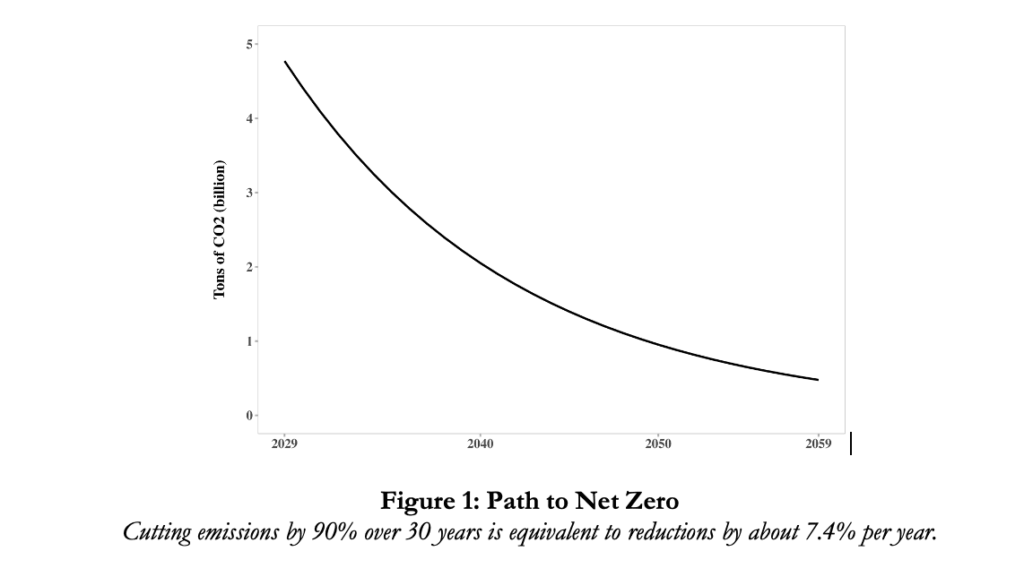

We can easily figure out what we need to do to reach net zero emissions. Figure 1 shows the path that would reduce emissions by 90 percent in the three decades beginning when the next President takes office in 2029, at the steady pace of 7.4% per year. A 90 percent reduction can be taken as a reasonable approximation to net zero if we assume that negative emissions strategies, such as enhanced carbon sequestration in soils, grasslands, and forests, account for the remaining 10 percent.

Committing to this path would almost surely mean consciously curtailing the supply of fossil fuels. The demand-side efforts on which the U.S. has largely relied to date have failed to produce anything near this rate of emissions reduction. Since U.S. carbon emissions peaked in 2007, the average rate of decrease has been only 1.5 percent per year. At that rate it would take 150 years to reach net zero, by which time climate destabilization will have inflicted enormous harm.

Curtailing the amount of fossil fuels allowed to enter the economy to achieve the net-zero pathway would raise their prices substantially. Curtailing supply and raising prices is like telling kids, “Eat your broccoli.” It may not taste good, but it’s good for you. You have to do it. Anyone who ever sat across a table from a kid who doesn’t like broccoli knows it can be a hard sell.

Yet this is the only sure way to get on the path to net zero. Putting a hard limit on the amount of fossil carbon permitted to enter the nation’s economy solves the open-access problem—the hard-limit rule is a kind of property right—but it runs smack into the price conundrum.

The Carbon Dividend Solution

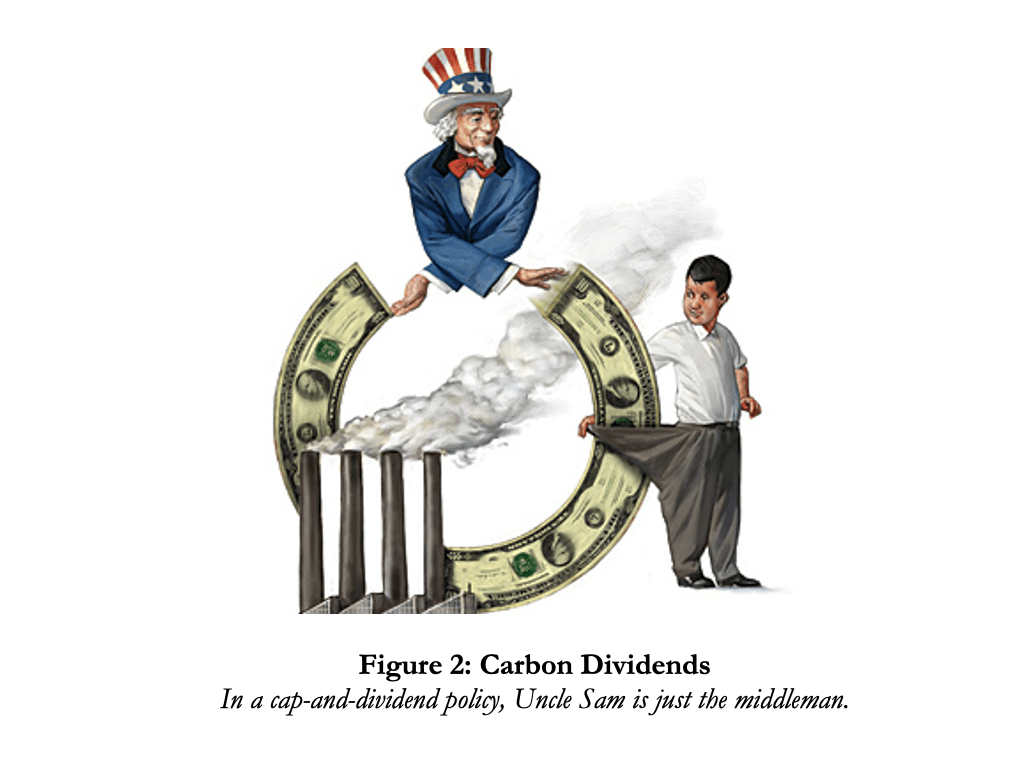

The best way to resolve this conundrum—in a democratic society, perhaps the only way—is to capture the money paid by the public in higher fuel prices and recycle it straight back to the people as equal per-person dividends. This can be done by auctioning the permits to the fossil fuel suppliers, the cost of which will then be passed onto consumers, and then returning the revenue to individual households in quarterly or annual payments. In this scenario, the newly created property right belongs to the people—not to the government and not to corporations.

No one can be certain how much fossil fuel prices will rise because of the hard limit. This will depend on multiple unknowns, including the pace of technological change in renewable energy and energy efficiency.

It is plausible, however, that in the first ten years of such a policy, the revenue per person in the United States would amount to roughly $2,500 per year. That’s for every man, woman, and child in the country, so for a family of four, we’re talking about $10,000 a year. For working people that’s real money.

The name for such payments is “carbon dividends.” They’re also called “carbon cashbacks.” They could also be called “climate protection dividends,” since the money comes from phasing out carbon emissions to safeguard the climate.

In 2019, more than 1,500 economists, including 27 Nobel laureates, signed a statement in favor of such a policy. That same year I published a book called The Case for Carbon Dividends. The idea has been around a while, yet most people have never heard of it.

Lessons of the Cap-and-Trade Debacle

To understand why, we need to revisit the cap-and-trade debates earlier this century. Three times cap-and-trade bills came up for a vote on Capitol Hill, and three times they failed. The last time one was the Waxman-Markey bill, which passed the House in 2009 but died in the Senate. These defeats were a huge setback for climate policy from which we have yet to recover. They brought caps on carbon emissions into disrepute. Politicians became afraid of any policy that would raise the price of fossil fuels.

Cap-and-trade had similarities to the carbon dividend solution I sketched above, but differences too. The basic idea was to limit the supply of fossil fuels, increasing their prices, which would change the behavior of businesses and consumers. Those are the similarities. But in cap-in-trade, you give away the permits, or at least a big chunk of them, to the fossil fuel corporations, free-of-charge, rather than compelling them to buy the permits at competitive auctions. As fossil fuel prices rise due to the limit on supply, firms that get free permits keep the money. The idea was that the resulting windfall profits would buy their acquiescence to a cap, bringing them into the climate bargain.

The strategy didn’t work. At the end of the day, the fossil fuel firms turned out to have a two-track strategy. Plan A was cap-and-trade legislation, but plan B was no legislation at all—and that’s what they really wanted.

It is worth pausing to think about how cap-and-trade would have played out. Windfall profits from permit giveaways would have accrued to shareholders in proportion to their stock ownership—mostly to the rich since they own most of the stock—including foreign shareholders. There would have been a market for permit trading, since some firms would want more than their initial handout and others less. Permit trading would have created opportunities for Wall Street and other traders to speculate and skim off some of the money paid by consumers, again disproportionately benefiting the wealthy.

That’s an option that enjoyed a fair amount of bipartisan support on Capitol Hill prior to Waxman-Markey, though not enough to pass a bill. And it’s the option that Democratic Party leaders stuck with until Waxman-Markey died in the Senate in 2010. After that the party line on climate policy became “carrots not sticks,” subsidies for clean energy rather than penalties for fossil fuels. That strategy eventually bore fruit in the Biden administration’s Inflation Reduction Act, but the results were disappointing in terms of bending the carbon emissions curve.

A second option, which also used to be popular on the Democratic side of the aisle, would be to auction the permits (or institute a carbon tax) and let the government keep the money and decide what to do with it. It could be spending on clean energy projects or the military, tax cuts for the rich or tax cuts for the poor, deficit reduction, you name it. It would depend on what legislators on Capitol Hill decide. This option may not be quite as popular today with liberals as it used to be.

The third possibility, the one that Peter Barnes advanced in his pioneering 2001 book Who Owns the Sky? and that I’ve been advocating ever since learning about it from him, is cap-and-dividend. This is the policy I’ve described. Instead of giving windfall profits to shareholders or letting the government use the money according to the priorities of the legislators of the day, cap-and-dividend returns the money to the public on an equal per capita basis. In this case, Uncle Sam is simply the middleman, collecting money from the permit auctions and passing it to the people, as depicted in Figure 2 below.

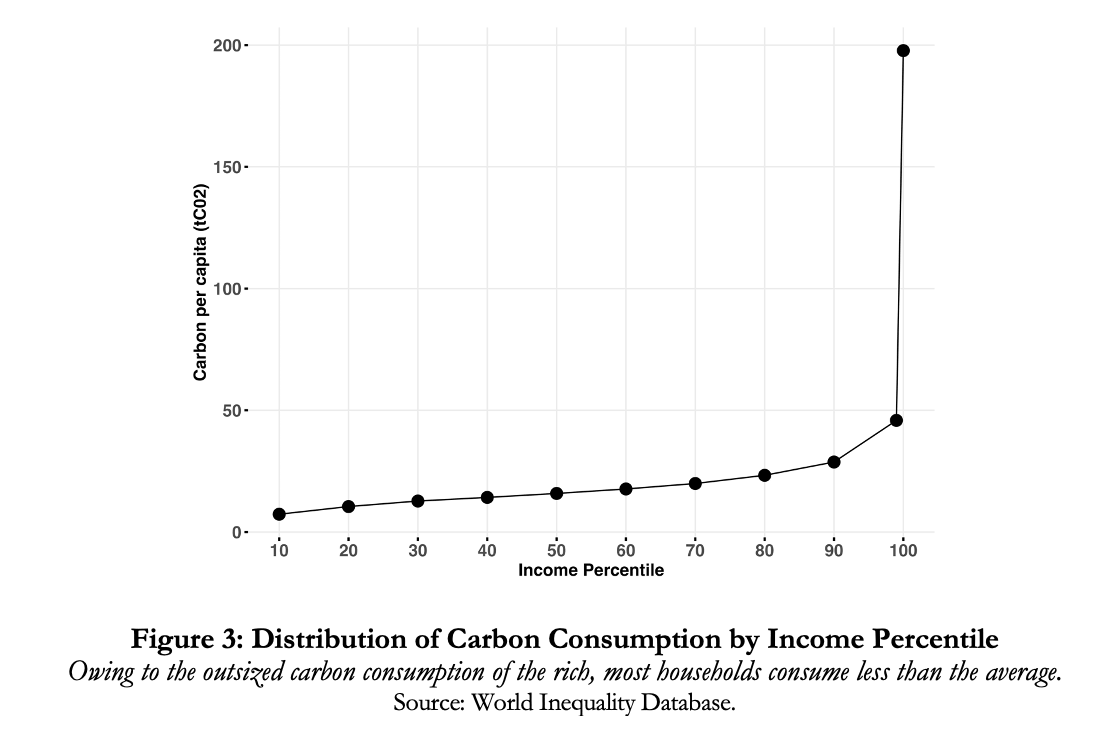

Distributionally, an attractive feature of dividends is that everybody gets the same amount back, whereas the effect of higher fuel prices depends on how much they consume. Most households—and the vast majority of working families—will get back more than they pay in higher prices. This is because about 75 percent of households consume less than the average amount of fossil fuels, the average being pulled up by the outsized carbon footprints of the rich (see Figure 3). Affluent households will pay more in higher fuel prices than they receive in dividends, but they can afford it.

The Politics of Carbon Dividends

The idea behind carbon dividends is that the limited carbon absorptive capacity of the biosphere belongs to us all in equal and common measure. It does not belong to corporations. It does not belong to the government. Instead, it is an example of what Tawney and Schumacher had in mind when they advocated “decentralized ownership of public property.”

Although this option did not carry the day among politicians during the cap-and-trade debates, there were notable exceptions. In 2009 two bills were introduced that proposed cap-and-dividend solutions. One was a House bill sponsored by then-Congressman Chris Van Hollen of Maryland. The other was a Senate bill introduced by Senators Maria Cantwell, Democrat of Washington state, and Susan Collins, Republican of Maine. The Democratic leadership made the fateful decision to bottle up both bills in committee, never bringing them to the floor—instead putting all its eggs in the cap-and-trade basket with lamentable results that we’ve been living with ever since.

Van Hollen, now a Senator, has continued to reintroduce updated versions of his bill every new session of Congress. It’s now called the Van Hollen-Beyer bill, because Representative Don Beyer from Virginia is its House co-sponsor. You can easily find the latest version online where bills and their legislative history are made public. It’s called the Healthy Climate and Family Security Act. If it became law, it would do exactly what I’ve described. Unlike Waxman-Markey, which was 1,400 pages long, Van Hollen-Beyer is just 29 pages long. There are no tradable permits to worry about: the firms buy the number of permits they choose at the auctions, so they don’t need to be tradable. If you have the patience to read through legislation, I recommend the Van Hollen-Beyer bill.

To summarize: The attractions of carbon dividends are, first, that working people get the money from higher fuel prices back into their own pockets and therefore can afford them. This can help build broad public support for the policy, something that was lacking in the case of the cap-and-trade bills. Second, it has a progressive distributional impact: it raises net incomes for working people, whose dividends exceed what they pay in higher fuel prices, while reducing net incomes at the top end of the spectrum. Finally, it embodies the ethical principle of universal, decentralized ownership of common wealth.

The major weakness of the policy—and the reason why so few people have heard of it—is that nobody gets rich from it. If nobody is going to get rich, nobody pays to lobby on its behalf, publicize it, or go to Capitol Hill and talk to Congresspeople about it.

This is not to say that it is politically impossible for carbon dividends to become a reality, but making it happen will require ordinary folks—people like you and me, people without deep pockets but with deep commitments—to organize and demand it. And that, of course, is a big ask. But saving the planet is a big ask too. We must rise to the challenge.

Universal Property

Carbon dividends illustrate a broader concept called universal property. Universal property has three core features. One is that it is individual—the property is owned by individuals, not by corporations or governments. Individuals own the resource—in this case, the carbon absorptive capacity of the biosphere—and individuals are paid for its use. Second, universal property is inalienable. It cannot be sold or transferred. It is a birthright, not a commodity. Third, universal property is perfectly egalitarian. Everyone has the same right to share in the fruits of its use. By putting flesh on the bones of the idea of decentralized ownership of public property, it fills what is largely a missing piece in our current structure of property rights.

It is not entirely missing, however. Universal property exists today in the state of Alaska. When corporations began pumping oil on Alaska’s North Slope in the 1980s, the Republican governor at the time, Jay Hammond, came up with the idea of the Alaska Permanent Fund. The underlying principle is that the oil belongs equally to all Alaskans. To put this principle into practice, the state government charges a royalty on every barrel of oil, deposits the money into the Permanent Fund, and taps that fund to pay equal annual dividends to every Alaskan resident. The size of Alaska’s dividends has varied over the years, but recently they’ve been around $2,000 per person. Not surprisingly, it’s a policy that enjoys wide public support across party lines.

This is an example of universal property. It has one crucial difference from carbon dividends, however: the money comes from pumping oil, not from keeping it in the ground. Many Alaskans would like to see their state pump more oil, because more oil means bigger dividends. In contrast, carbon dividends come from limiting the use of fossil fuels. Ratcheting down the supply is what generates the dividends.

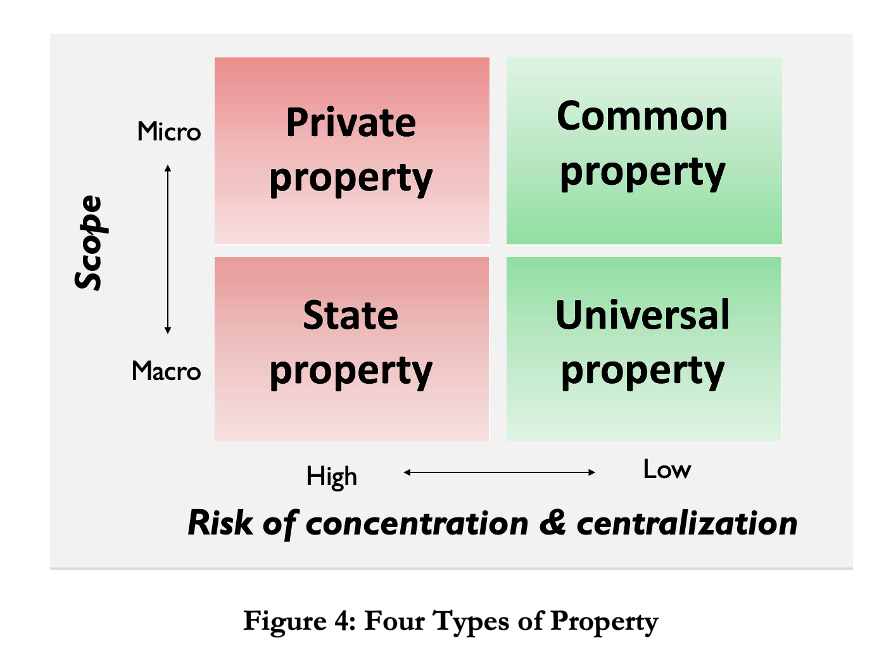

Figure 4 depicts four types of property defined in terms of their scope—whether they operate at the level of individual units or the system as a whole—and the risk of concentration and centralization, the pitfalls that Schumacher warned against in Small is Beautiful.

The first type, and most familiar, is private property. It is micro—it consists of individual units—but it comes with a significant risk of concentration in a few hands. This is not to say there shouldn’t be any private property, of course, but we need to guard against that risk.

The second type is state property. It is macro—at the level of the entire economy—but it too comes with a high risk of concentration, as Schumacher and Tawney warned. The centralization and concentration of state power can yield outcomes that are neither good for the environment nor good for most people.

The third type is common property, the importance of which has been illuminated in recent years by many authors including Elinor Ostrom and David Bollier. Common property again operates on the micro level, in this case at the level of communities rather than individuals. Traditionally, it has been used most often to govern the use of natural resources such as water, grazing lands, fisheries, and forests. Compared to private property and state property, it has a relatively low risk of concentration and centralization.

Finally, we have universal property, which with a few exceptions like the Alaska Permanent Fund is almost an empty box. Like state property, universal property is at the macro level, pertaining to the economy as a whole. It combines bigness—in this sense—with low risk of concentration and centralization. There is no risk, in fact, as long as its core tenets of individuality, inalienability, and egalitarianism are firmly in place.

Universal property makes the idea of decentralized ownership of public property into something real. This possibility—that has been like a dormant seed in the literature on property rights since Tawney and Schumacher planted it—is primed to blossom today.

Some years back, when visiting the Ministry of Public Education in Mexico City, I came upon a remarkable mural by the great Mexican artist, Diego Rivera. Across the bottom of the mural was an inscription he had written. It reads, “The land belongs to all, just like the water, the light, and the heat of the sun.” The notion of universal property is widely shared across cultures around the world, and it could be made operational not only here but everywhere.

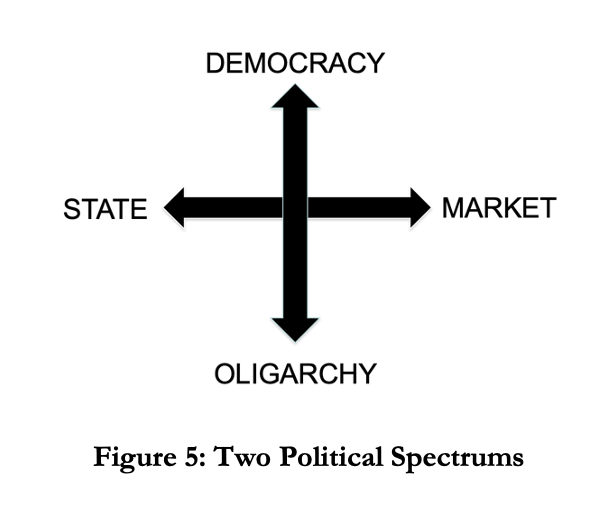

Today we are accustomed to defining the political landscape in terms of “left” and “right.” Our understanding of what these terms mean dates from the late 1700s and early 1800s, and centers on the balance between the market and the state, the right being more pro-market and the left more pro-state.

I would suggest that there is another political spectrum, however, that is at least as important, perhaps more so. It is the spectrum between democracy on the one hand and oligarchy on the other. The spectrum is at right angles to the state-market axis, as shown in Figure 5. It is not a defining feature of the conventional left-and-right distinction. The right tends to conflate the market with democracy and the state with oligarchy, while the left applies the reverse spin and tends to conflate the market with oligarchy and the state with democracy. But I submit to you that no matter how you strike the balance between market and state, there is no guarantee of a democratic outcome.

The key issue is: are wealth and power concentrated in the hands of a few, or are they widely dispersed among the people? That is a difference that profoundly shapes how states and markets function in the real world. In an oligarchic setting, no matter the mix of market and state, we can expect to see outcomes that are bad for the environment and bad for most people. In a democratic setting, it is more likely, if not inevitable, that we will get better outcomes. That, I believe, is the spectrum we ought to keep first and foremost in our minds when we’re talking about politics.

Louis Brandeis, the distinguished Supreme Court Justice of the early 20th century, once said, “We must make our choice. We may have democracy, or we may have wealth concentrated in the hands of a few, but we cannot have both.” I think that sums it up.

Today in the United States we are witnessing a consolidation of oligarchic rule. This is sometimes described as a movement towards fascism—and I think there is a connection between oligarchy and fascism. Both are pathologies of the body politic. In the language of toxicology, exposures that are not enough to kill you, but just make you feel sick, are called chronic. And if the toxic exposure threatens to kill you, it’s called acute. Fascism is the acute version of oligarchy, and I truly hope we don’t get to that point.

To conclude, universal property can help to bake democracy into the structure of property rights. It can help to maintain a level playing field, one that cannot be eroded over time—and indeed could expand as more assets become incorporated into its realm. Carbon dividends are a good place to start, because they would address one of the most urgent environmental challenges of our time. But they could be the beginning, not the end, of what could eventually emerge if universal property takes its rightful place alongside private, state, and common property. Universal property would help to correct two fundamental flaws of all modern economic systems, wherever they fall on the market-state axis: unbridled inequalities of wealth and power, and the degradation of our natural environment.

My advice is to go for it.

Thank you very much.