The growing local currency movement is providing a positive way to respond to the alienation from the natural world fostered by an expanding global marketplace, and to restore the possibility of regional economies based on social and ecological principles. In a simple barter economy, production methods are highly visible. The value of the carrots we offer in trade is directly related to our memories of hoeing in the garden, of building the compost pile, and of waiting for the rain after planting. And though our picture of the cordwood for which we are bartering is not as detailed, still we probably have seen our neighbor as he split and stacked the wood from the ash tree. Barter transactions link us inextricably to a particular place and time.

- Susan Witt in Small is Beautiful: Economics as if People Mattered: 25 Years Later... With Commentaries

The Schumacher Center for a New Economics employs the term “local currencies” to refer to place-based monetary tools for building sustainable local economies. Other terms that have arisen include “complementary currencies,” “community currencies,” and sometimes “alternative currencies.” These local currencies take many forms.

The variety of local currency programs reflect three very different kinds of money. One is purchase money that facilitates the ability or individuals to transact for needed goods and services. Purchase money, the lifeblood of any economy, is a record of our economic exchanges with one another. The second is gift money recording our generosity to others. The gift economy builds very real links in a community, strengthening the social and cultural fabric and contributing to the quality of life, but does not directly enter into the creation and exchange of goods and services.

The third kind of money is what is commonly known as investment capital. This is money needed for business start-ups and expansion, capital tor the means of production as distinct from monthly operating costs. Investment capital can come from surplus income saved and then reinvested in new enterprises, or it can come from the actual creation of new money at the point of making a loan. When Jane Jacobs, the renowned regional planner, portrayed regional currencies as an elegant tool for community creation of import-replacing businesses, she had this power to create new money in mind.

The goal of the Schumacher Center for a New Economics’ local currency program is to demonstrate how regional communities can issue their own money to finance local production and build sustainable local economies.

- Historic Local Bank Notes

- Convertible Paper Currencies

- WIR

- HOURS

- Time Dollars, Time Banks

- LETS and Mutual Credit Systems

- Self-financing Scrip

- Multiple-store Notes/Customer Loyalty Scrip

- Commodity Backed Currencies

- Barter Exchange Systems

- Electronic Trading Tools

- BlockChain Currencies

- Future of Local Currencies

Historic Local Bank Notes

In the 1800s nearly all commercial banks in the United States issued their own individual currencies at the point of making “productive” loans to businesses. Typically, a productive loan is made for the purchase of equipment (machinery, tools, supplies) that will result in an increased availability of goods in the economy. The upshot of such a disciplined issuing policy is a currency that holds its value. Local issue meant that it was local bankers who determined the amount and kind of credit needed to stimulate business development in each particular region.

In the 1800s nearly all commercial banks in the United States issued their own individual currencies at the point of making “productive” loans to businesses. Typically, a productive loan is made for the purchase of equipment (machinery, tools, supplies) that will result in an increased availability of goods in the economy. The upshot of such a disciplined issuing policy is a currency that holds its value. Local issue meant that it was local bankers who determined the amount and kind of credit needed to stimulate business development in each particular region.

In 1913 with the creation of the Federal Reserve Act, local bank money was replaced by the federal dollar issued by a coalition or private banks that make up the Federal Reserve banking system. The International Independence Institute, under the leadership of Ralph Borsodi and Schumacher Center founding President, Robert Swann, issued a “Constant” in Exeter, New Hampshire in 1972 in cooperation with an Exeter bank. The Constant circulated for a year in Exeter stores as a demonstration that local bank notes, working with the not-for-profit sector, remain a contemporary option for local exchange.

Read Ralph Borsodi’s “Inflation and The Coming Keynesian Catastrophe: The Story of the Exeter Experiments With Constants” to learn more about the “Constant”.

Read an account of the island of Guernsey's locally issued currency to learn about local municipalities using local currency. Then read Susan Witt's proposal for how this model might be applied to municipalities in the United States.

Convertible Paper Currencies

Today multiple communities around the world have issued their own currencies in cooperation with local banks. These currencies circulate parallel to, rather than as a replacement for, the national currency. The currencies are typically easily recognizable colorful notes that exchange at a fixed rate to the national currency.

Today multiple communities around the world have issued their own currencies in cooperation with local banks. These currencies circulate parallel to, rather than as a replacement for, the national currency. The currencies are typically easily recognizable colorful notes that exchange at a fixed rate to the national currency.

One of the most successful programs is BerkShares in Berkshire County, Massachusetts. In 2006 the Schumacher Center for a New Economics worked with businesses, banks, and private citizens in its home region of the Berkshires to incorporate BerkShares, Inc. Organized as a non-profit corporation with membership open to anyone in the region, the board of directors is elected by members at an annual meeting. BerkShares, Inc. designed and printed BerkShare notes (B$), which feature local heroes and the works of local artists. The B$ were then distributed to the 16 branches of four local participating banks where they are held on reserve. Citizens can exchange federal dollars for B$ at any of the 16 branch banks at $95 for 100 B$. The federal dollars are held in BerkShares, Inc. accounts at the banks to back the notes in circulation.

To learn more, read Susan Witt’s essay Democratizing Monetary Issue: Vision and Implementation in the Berkshire Region of the U.S

Other successful examples of convertible paper currencies working in cooperation with local banks include the Chiemgauer in Germany and the Bristol Pound in England. Chiemgauer is the oldest and most robust. In addition to having an electronic component, it incorporates demurrage (a tax on the currency that devalues it over time) which is used to encourage spending rather than hoarding.

New legislation in some European countries has encouraged the proliferation of convertible paper currencies issued by business associations. Some have additionally included electronic exchange platforms. Most are not issued through banks, but rather at exchange points hosted by businesses. Reserves in the national currency are maintained to accommodate redemption.

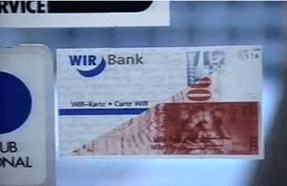

WIR

Because WIR is unique and incorporates multiple facets of other currencies, it has its own place in this list of models.

Because WIR is unique and incorporates multiple facets of other currencies, it has its own place in this list of models.

In 1934, Basel, Switzerland became headquarters to a highly successful Swiss business to business barter exchange system known as “WIR,” (German for “We”). Consumers at first were excluded from participation. Trades were denominated in WIR and businesses could “bank” credits for future transaction. Trades were recorded with a signed receipt, much like a credit card receipt, and then sent in to a centralized administrative office for recording. A. percentage of each transaction paid for administration of the program.

Members were and are given discount incentives for trading within the system. Regional exhibits of businesses accepting WIR are held throughout Switzerland and colorful, glossy catalogues list products. Businesses with accumulated WIR attend these exhibits and study the catalogue to decide how to allocate their supply. WIR are not convertible to Francs and so must be spent within the system. System administrators are authorized to extend credit (make loans in WIR) to businesses meeting the system’s economic criteria.

More recently WIR created a bank that permits deposits in Swiss Francs at competitive rates. Consumer/depositors can then change their Francs into WIR and spend them at retail sites that accept WIR, indicated by signs in windows. Loans are made in combinations of Swiss Francs and WIR. Turnover of WIR is in the billions annually. Most all of the trades have contracts that include a portion of payment in WIR. The WIR network is credited with stabilizing the Swiss economy.

To learn more about WIR:

Read the 1977 WIR Report by Erick S. Hansch

Read “60 Years of the WIR Economic Circle Cooperative” translated by Frederika Almstedt (with editorial assistance from Thomas Greco). First appeared in WIR Magazin, September 1994.

Watch this video

HOURS

In 1991, after researching local currency issue at the Schumacher Center’s Library, including long conversations with Bob Swann, Paul Glover organized a local currency for his hometown of Ithaca, New York. This currency used paper notes for the trade of local goods and services, and the notes were denominated in hours of labor (equivalent to the average hourly wage for Ithaca or $10). To begin circulation, Ithaca Hours were given in amounts of 4 hours to owners or small businesses willing to accept the notes in trade for goods and services. Paul’s concept was that Hours would be backed by the future productivity of those to whom they were issued and so Hours would maintain a strong value independent of the fluctuation in federal dollars.

In 1991, after researching local currency issue at the Schumacher Center’s Library, including long conversations with Bob Swann, Paul Glover organized a local currency for his hometown of Ithaca, New York. This currency used paper notes for the trade of local goods and services, and the notes were denominated in hours of labor (equivalent to the average hourly wage for Ithaca or $10). To begin circulation, Ithaca Hours were given in amounts of 4 hours to owners or small businesses willing to accept the notes in trade for goods and services. Paul’s concept was that Hours would be backed by the future productivity of those to whom they were issued and so Hours would maintain a strong value independent of the fluctuation in federal dollars.

Over the next decade, Hours programs spread in over 50 communities throughout the United States and Canada engaging citizens in the discussion of creating their own regional monetary systems. Of these start-ups only a few are still running.

One factor in the attrition of Hours programs is that community groups failed to anticipate the start-up time and costs involved in promoting and sustaining a new currency issue.

Time Dollars, Time Banks (UK)

Following a long illness during which the services or others were critical to his recovery, lawyer Edgar Cahn devised a program called Time Banking. Time Dollars are used to record the good deeds of neighbors for each other. Old, young, handicapped, and marginalized, all have some service to contribute to their community and so can earn and bank Time Dollars for occasions when they are in need. In order for Time Dollar Institutes to maintain tax-exempt status as charities. Time Dollar transactions are generally limited to what would be called “the gift economy,” excluding commercial economic exchanges. Nevertheless, Time Dollars have shown to be an extraordinary tool for weaving values such as reciprocity, trust, cooperation, and what Edgar calls ”co-production” in a community. Numerous Time Dollar Networks are active throughout the US and the UK.

Following a long illness during which the services or others were critical to his recovery, lawyer Edgar Cahn devised a program called Time Banking. Time Dollars are used to record the good deeds of neighbors for each other. Old, young, handicapped, and marginalized, all have some service to contribute to their community and so can earn and bank Time Dollars for occasions when they are in need. In order for Time Dollar Institutes to maintain tax-exempt status as charities. Time Dollar transactions are generally limited to what would be called “the gift economy,” excluding commercial economic exchanges. Nevertheless, Time Dollars have shown to be an extraordinary tool for weaving values such as reciprocity, trust, cooperation, and what Edgar calls ”co-production” in a community. Numerous Time Dollar Networks are active throughout the US and the UK.

Variations on the TimeBank model include the Red Sostenible & Creativa in Spain, which uses a Social Coin seeking "to foster solidarity and camaraderie through chains of favors."

LETS (Local Economic Trading Systems) and Mutual Credit Systems

Michael Linton founded the first LETS program in the early 1980s on Vancouver Island in Canada. LETS programs were created as a simple debit and credit system, denominated in the national currency. Consumers wishing to purchase goods or services offered through the LETS program would simply phone in a transaction to a central coordinator and their LETS account would be debited and the seller’s account credited. Producers would then spend their credits with other members in the system. The system was essentially self-regulated with members issuing their own line of credit at the point of making a purchase.

LETS programs are by far the most popular local currency systems throughout the world, spawning various adaptations, and facilitated by customized computer programs. (See Cyclos software designed by Henk van Arkel of the Social Trade Organization in the Netherlands.)

LETS development has been slow in the US, however. IRS law recognizes LETS programs as barter systems and as such requires system managers to report the total value of transactions for each individual to the Internal Revenue Service. This kind of management has proven costly and burdensome for start-up systems, discouraging broad replication in this country up until this point.

Self-Financing Scrip

In 1989, after being denied a bank loan, the owner of The Deli in Great Barrington, Massachusetts, turned to the SHARE microcredit program organized by the Schumacher Center for a New Economics for a loan. SHARE staff recommended that he borrow from his established customers instead. As a result, Frank Tortoriello issued “Deli Dollars” as a way to finance the move of his business from one location to another. Customers bought Deli Dollars for $8 to be redeemed for $10 worth of soup and sandwiches at a later date. It was not the first time scrip had been used as a self-financing tool for a small business, but Deli Dollars caught the attention of international media including CNN, NBC, CBS, and Tokyo TV, giving new energy to the local currency movement. Other small businesses in Great Barrington issued their own notes to eager customers, demonstrating that citizens working together can create independent, low-cost methods or making micro-credit loans that double as a local currency.

In 1989, after being denied a bank loan, the owner of The Deli in Great Barrington, Massachusetts, turned to the SHARE microcredit program organized by the Schumacher Center for a New Economics for a loan. SHARE staff recommended that he borrow from his established customers instead. As a result, Frank Tortoriello issued “Deli Dollars” as a way to finance the move of his business from one location to another. Customers bought Deli Dollars for $8 to be redeemed for $10 worth of soup and sandwiches at a later date. It was not the first time scrip had been used as a self-financing tool for a small business, but Deli Dollars caught the attention of international media including CNN, NBC, CBS, and Tokyo TV, giving new energy to the local currency movement. Other small businesses in Great Barrington issued their own notes to eager customers, demonstrating that citizens working together can create independent, low-cost methods or making micro-credit loans that double as a local currency.

Multiple-Store Notes/Customer Loyalty Scrip

In 1991 in Great Barrington, seventy merchants worked with the Chamber of Commerce to issue Berk-Shares. During a six-week period, customers collected one Berk-Share for every $10 spent at one of the stores. Then during a designated three-day redemption period, Berk-Shares could he spent as cash for store items, creating a spirit of festivity on Main Street. There are many variations on this simple approach in which multiple businesses incentivize their regular customers through reward programs.

In 1991 in Great Barrington, seventy merchants worked with the Chamber of Commerce to issue Berk-Shares. During a six-week period, customers collected one Berk-Share for every $10 spent at one of the stores. Then during a designated three-day redemption period, Berk-Shares could he spent as cash for store items, creating a spirit of festivity on Main Street. There are many variations on this simple approach in which multiple businesses incentivize their regular customers through reward programs.

In some parts of Canada, merchants partner with banks to make low-interest loans during the holidays in local scrip. The scrip can only be spent at local stores, discouraging online shopping and returning trade to the face-to-face transactions of Main Street shops.

Commodity Backed Currencies

For centuries fiscal conservatives have advocated for a currency backed by something of perceived value such as gold and silver as a way to discourage the over-issue that leads to inflation. The Liberty Dollar is a contemporary private, for-profit revival of the effort to create a gold and silver backed currency. However as the minting of coins is prohibited in the US, the Liberty Dollar was shut down.

For centuries fiscal conservatives have advocated for a currency backed by something of perceived value such as gold and silver as a way to discourage the over-issue that leads to inflation. The Liberty Dollar is a contemporary private, for-profit revival of the effort to create a gold and silver backed currency. However as the minting of coins is prohibited in the US, the Liberty Dollar was shut down.

Others have suggested backing in a basket of commodities such as grains, vegetable oils, fossil fuels, and minerals. In the town of Exeter, New Hampshire, the economist Ralph Borsodi and Robert Swann issued a currency that was based on a standard of value using thirty different commodities in an index similar to the Dow Jones Average. It was called the Constant because, unlike the national currency, it would hold its value over time. Read Ralph Borsodi’s “Inflation and The Coming Keynesian Catastrophe: The Story of the Exeter Experiments With Constants” to learn more about the “Constant”.

Buckminster Fuller recommended valuing currency in kilowatt hours since all production requires energy. Of course, he imagined a system of distributed production of green energy as a way to back such currency.

Barter Exchange Systems

Our earliest experience of barter is the simple exchange of goods or services between two people. However, there is a thriving international world of commercial barter exchanges. These systems can involve complex multiple trades. While most of these systems denominate trades in US dollars, some are introducing their own measure of exchange functioning much l ike a currency.

Other barter groups rely on inventories of excess capacity, offering these inventories in trade at discounts to members. Some commercial barter groups are considering ways to expand their trade to include consumers, thereby functioning as a currency within a defined trading arena.

Electronic Trading Tools

The Internet and other new technologies such as “smart cards” have opened the possibility of trading without use or traditional forms or money. Many inventive individuals are suggesting ways or linking these electronic cards, which are primarily tools to facilitate consumer credit, to businesses with defined missions, such as merchants of green products.

The Internet and other new technologies such as “smart cards” have opened the possibility of trading without use or traditional forms or money. Many inventive individuals are suggesting ways or linking these electronic cards, which are primarily tools to facilitate consumer credit, to businesses with defined missions, such as merchants of green products.

The electronic systems are, for the most part, internet versions of mutual trading systems relying on debits and credits to track exchanges. Different systems set their own rules and governance structures, such as limits to how much members can go into debt, or geographical borders for trade, or even nature of goods traded. Cyclos remains one of the most versatile and utilized independent software platform for such currencies.

BlockChain Currencies

The introduction of currencies built on blockchains has opened the door to new fluidity and innovation in payment systems. Mostly for-profit, and primarily global in aspiration they promise to facilitate transactions for pennies in contrast to credit card fees. Bancor is a blockchain currency that provides a platform for regional currencies to operate and design their own governance systems. Holochain, another customizable and decentralized blockchain currency can record multiple kinds of transactions including what would normally be thought of as in the gift economy and reputational currencies.

The introduction of currencies built on blockchains has opened the door to new fluidity and innovation in payment systems. Mostly for-profit, and primarily global in aspiration they promise to facilitate transactions for pennies in contrast to credit card fees. Bancor is a blockchain currency that provides a platform for regional currencies to operate and design their own governance systems. Holochain, another customizable and decentralized blockchain currency can record multiple kinds of transactions including what would normally be thought of as in the gift economy and reputational currencies.

Future of Local Currencies

What should we expect from the local currency movement in the near term?

(1) Certainly new motivation in consumer-credit systems—supporting “Buy Local First” programs, and providing incentives tor consumers to come back to the storefronts on their Main Streets.

(2) Greater cooperation between the highly popular Time Dollar systems and the consumer credit systems in which administrative capabilities are shared, outreach in the local community is shared, and technology is shared.

(3) At the same time, it will be essential to apply our collective creativity to the problem of how communities can issue local currencies in the form of no-interest loans to finance businesses producing goods now imported from afar.

In the future, all three forms of money--purchase money, gift money, and investment money--will be essential to an overall strategy for building healthy local economies.