First of all I want to thank the Schumacher Center for a New Economics for inviting me to speak. I also want to remind us of and recognize the pioneering work the Schumacher Center has done to try and bring to economic life not just human scale but a sense of sanity when we are rapidly losing both. I am not a devotee of Fritz Schumacher—I heard him speak twice in England—but I am very respectful of his approach. Although I’m not sure how he would have reacted to what I’m going to say, I thought I should make my relationship to him clear at the outset.

I would like to put in a good word for the Schumacher Center, which I may do because I’m not part of the organization. It has occurred to me that many of the larger movements which have now developed in the United States, such as the Bioneers, indirectly owe their origin to a certain extent to Schumacher’s thought and to the Schumacher Center, which has transmitted his ideas. I do not speak on behalf of the Schumacher Center, but it is a concern of mine that, to be fair, those who have been inspired by these ideas and then go on to develop them should remember where they came from. By this I mean it would be a fine thing if those on the sustainable development road were to part-tithe funds to the Schumacher Center. It’s easy for younger organizations to reach the point where they forget their mother. They tend to eclipse their starting point, forcing the mother into the circus of fundraising, which, with no insult intended to any fundraisers present, can be quite demeaning and has become increasingly problematic. Gandhi had an interesting concept of fundraising. He was quite clear that the best fundraising is done by persuading people to consistently send small amounts of money to an organization rather than by banging on doors for big lumps of capital.

I wanted to make this plug for the Schumacher Center because I think part of the story of taking ownership of governance is to also take ownership of the monetary effects we can have. One of them would be to remember the Center financially, to lessen its need to go banging on doors. I’m saying this completely off the cuff, unprompted, and without permission. I hope I’m not being out of order.

Another thing I want to say by way of introduction is that I’m going to give this talk mindful of a colleague of mine, Joel Kobran, who died a few days ago and who spent much of his time concerned with the questions I shall talk about.

Now, I’m quite on edge, for what can I say about local currencies to a gathering like this? What has not already been said or even done in this area? I don’t want to bring coals to Newcastle, so I’m not going to revisit the whole discussion about local currencies but instead will present three concerns I have. First, I’m concerned that the take-up of local currencies is not fast enough and not vast enough, considering the events we’re now experiencing in the financial world. I do not mean to gainsay the local currency movement, but I do worry that it may prove to be of no consequence because of the macro situation now prevailing, both geopolitically and conceptually. Second, I’m not at all sure how helpful it is to speak in antithetical terms of “us” and “them.” The third concern I have is whether the analysis of the local currency movement and therefore the remedies it is meant to bring are historically and technically accurate enough. I say this because if they are not historically or technically accurate, I don’t believe they will have the effect they could otherwise have in terms of the larger picture.

The Role of Imagery

An unspoken secret about economics is that it relies entirely on images, even though it uses words a great deal. I’d like to mention a few of these images to give you an idea of what I mean.

An image occurs to me that is part Greek, part Wild West, an image I have because my whole life has been spent between the Greek islands and California. It is an image that, at least to my mind, is relevant to the modern financial and monetary situation: Humanity is faced with wild horses that are running ahead of it and are beyond its control. The question is how to capture these wild horses. How do we manage this problem? In the National Museum in Athens there is a statue of a young charioteer, an elegant figure standing very upright, as if with reins in his hands, the reins of the horses in front of his chariot. He is managing these wild horses by looking straight ahead into the distance; he knows exactly what they’re up to, but he’s not giving them his direct attention. This is an important, albeit ancient, image. If I go to the Wild West, I have the image of a herd of mustangs rushing past. I’m trying to catch up and jump onto one of these crazy horses in cowboy fashion. My point is that, with the modern monetary situations we are faced with, this image of humanity trying to master wild horses is a highly relevant one.

If you’re a modern economist, you can’t function without the image of an invisible hand. That is an extremely strong image. If you ever try to draw it, you’ll have quite a challenge! Once I gave a workshop where the task was to draw the invisible hand. I’ve also been to a workshop where we played charades. I came on carrying my briefcase, with my hand up my sleeve and a piece of thin nylon thread between me and the briefcase handle. The others had to guess what I was depicting. The image of the invisible hand is the basis of modern economics, which is completely disingenuous because modern economics prides itself on being completely rational. But what is rational about an invisible hand? The third image I want to mention is that of liquidity and therefore of flow, without which economics would collapse like a toy donkey without its string.

These examples illustrate that modern economics, including the more abstract versions of it, would not exist were it not for images of this kind. In addition to pointing out the extent to which economics relies on imagery I also want to show how a different kind of imagery can take economics further, releasing a different potential from what we’re used to. With imagery, you can do something that you cannot easily do with words: You can take any audience beyond its language, beyond its culture, beyond its nationality and into a universal domain. My work takes me all over the world into many settings, from the Green Party monetary policy committee sitting in a field in Kent in summer to the inner sanctum of the Bank of England. It’s challenging to be moving among many different cultures, up and down within a society as well as across the world into different language spheres yet all the time to be telling the same story. The easiest way to go about it is to enter the realm of images, for every human being can understand images when words cannot be understood. This is because almost every word that is said signals something else to a different person, to a different audience, and so on.

Another thing I want to say about images concerns the picture we have of the United States. I have felt for a long time that it would help the whole of humanity if we asked, What is the United States of America from a humanity-wide point of view? A good deal of what was said earlier today by Nancy Jack Todd and Thomas Linzey has urgency for all humanity. For example, if you start changing or modifying your Constitution, you need to take into account the whole of humanity because from a certain point of view most of the world is now focused on the United States. If you start tweaking your Constitution, the rest of the world will be watching carefully because the American people are part of all humanity.

Recently I wrote a little book called Rare Albion. Because I was commissioned by an American to write it, I gave it an American setting. I thought of how perennially popular the movie The Wizard of Oz is, so I subtitled my book The Further Adventures of the Wizard from Oz. The story is about America, but I renamed it the Confederated States of Columbia, for reasons I won’t go into. Rare Albion is the island capital of the Confederated States of Columbia, analogous to the District of Columbia. This is a way of describing the whole world as linked to the United States. I think this metaphor plays a major role in what I’m going to discuss in monetary terms. Human beings need somehow to go to an imaginary place if they are to move from where they are now to where they should be, and this can be done with the help of imagery. We need to come out of our immediate context in order to stand in another one. And in the realm of metaphor, of imagery, I think there’s a universality that we need to access.

Now I’d like to use my traveling blackboard [a large sheet of black paper] to illustrate what I’m going to say. I use this blackboard for a couple of reasons. First, I am an economist, and that means I am a dismal person, so I’d like to do my bit to rescue the reputation of economics by making it a little less dismal. I don’t pretend that this will be art, but it does add an artistic touch, such as is often needed.

I want to consider a key idea represented by the phrase “Think Globally, Act Locally.” I won’t discuss how this idea is understood in general, but I shall describe how I understand it.

To think locally is to think from me outwards. It means I am the center of the universe. Whatever my circumstance, I look at the world from me outwards. This is an image of “being local.” If I want to think globally, it’s the reverse: I need to think from the world to myself. This image has to do with the “us vs. them” concept. I don’t buy into us vs. them, but I do buy into “I can be conscious of my actions from here outwards, and if I choose to do so, I can also observe the effect I have on the world.” You don’t need to get together with me in order for me to think that way; I’m quite capable of thinking on behalf of humanity. To act locally but think globally comes down to whether I can observe the effects of my actions, thereby enabling myself to modify what I do. This is a crucial concept in economics. It takes us away from our egotistical activity toward a more other-minded way of working.

Modern economics is all about individualism, all about acting in one’s own name, yet that is a myopic, immature understanding of economic life. Modern economics also has to do with acting in the name of humanity, with me caring about the fate of the victims of Hurricane Katrina, for example. I don’t need someone to tell me to be concerned about them. As a human being I do not need external prompting to send relief money. An important part of modern economics is the recognition that what we discuss in such contexts as this we discuss precisely because the human being can be concerned about other people without having to be incited to be concerned.

Money and Credit

There are two aspects of the monetary world I want to talk about: money issue and credit creation. These are the key issues, whether on the level of a local currency or of Alan Greenspan as the Chairman of the Federal Reserve. His concern is focused on specific questions: Who issues money and how do we manage it? Where does credit come from and how do we understand it? Whatever context you’re in, these questions do not change. The perspective is different, but the technical problem is identical.

For me, money and credit are not the same thing. I see them as two separate worlds, and they should not be conflated. If they are, many problems arise. To put this into understandable terms, money is a reflection of the way we behave. It comes into being when people buy and sell things. This is pretty obvious in the example of a Local Exchange Trading System, known as LETS. In a LETS we issue money by buying something; moreover, when we buy and sell things, we’re meeting one another’s needs. This is rock solid economics: Money is related to meeting one another’s needs. And it is done through trade.

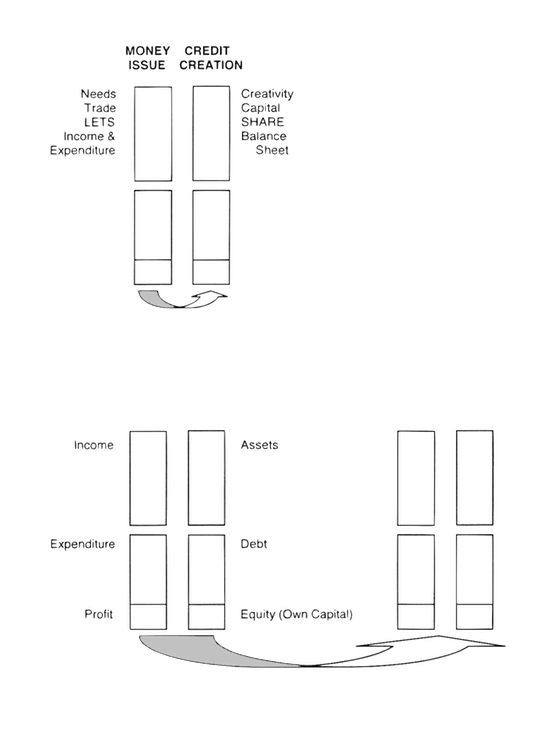

When we create credit, that is a whole other world. Contrary to the view most people have that credit is created by the central bank or by a consortium of private bankers unfairly charging the government, technically credit is created by people borrowing and lending. If I need to borrow to start a local bakery, the fact that I borrow engenders the creation of credit. Leaving aside the fact that normally I have to go to a bank to get it, the bank will not create credit if the baker doesn’t come in and say, “I want to start a bakery.” It’s important to see that the creation of credit is linked to lending and borrowing and that this is done in order to finance initiatives that result in the creation of new values, new wealth. Creativity is the link to credit. We have money and credit, we have the meeting of human needs (food, shelter, and so on), and we have the financing of initiatives people want to take in life. We can also say “trade” and “capital” as our two distinct, separate categories. So to the left of the blackboard sketch we have money/needs/trade, and to the right we have credit/creativity/capital. [The color sketches are reproduced below as line drawings in black and white.]

What’s essential in this story is to keep these two realms distinct. Most monetary problems begin when we don’t understand the difference between money and credit, between meeting human needs and financing human creativity. It helps our awareness of this difference if one does a bit of color-coding, dyeing the monetary world. The column on the left is the money side; everything to do with money I’m coloring red. The right column, the side of credit, I’m coloring blue. Color, being a step away from black and white, takes us beyond our normal thinking and gives an artistic link to our subject. It’s a strange experience to be with people who have understood this long enough that when they start talking about red and blue money, it is a completely coherent concept for them—born out of an inner sense, not out of conceptual discussions among economists.

LETS, SHARE, and Accounting

A further step in my argument here is to point out that in reality both the issue of money and the creation of credit are done by sovereign individuals. When I want to buy something, that’s my business. Nobody tells me to go and buy a loaf of bread; it’s my choice. When I want to borrow money, that’s my business also. I’m sovereign in these matters. But there can be no trade, there can be no economy on the basis of the sovereign individual alone. Economic activity requires me to operate in conjunction with other individuals. Thus, all money issued and all credit created are by definition the result of sovereign individuals working together. Whether we see this or not, understand it or not, it’s an inescapable piece of economics. You cannot have your hair cut in a barber shop if there’s no barber there. No trade, nothing in economic life, takes place in Robinson Crusoe fashion. In economic life it is an illusion to think one is alone and acting unto oneself.

In the complementary currency world, a local exchange trading system like LETS typically means that people use their post-tax income to trade with one another. They usually do not trade pre-tax but rather use their disposable income. The Internal Revenue Service says: “If you want to use your money in that way, it’s up to you, but do it with post-tax income. Then you can call your money whatever you want to call it; it’s irrelevant from our point of view.” I was involved with a LETS for a number of years in Canterbury, where the money was called “Tales,” believe it or not. If you looked at the system in detail, you would see that it was the accounts of people buying and selling. When someone buys a haircut, in accounting terms what you have is an income/expenditure transaction between two members of the LETS community. This is enormously important—the powerful and real link to accounting.

The Schumacher Center, on the other hand, initiated a micro-lending program called Self-Help for a Regional Economy (SHARE). I admit to not being aware of all its dimensions, but as far as I can tell it belongs on the credit side of my drawing. Not how do you pay for a haircut, but how do you capitalize a business? It’s interesting to me that the Schumacher Center is concerned with the credit side of things. When you try to capitalize something through a LETS system, it tends to become too complicated and, in my experience, the participants often don’t understand credit. But credit is on the right side of my drawing. This side is the balance sheet. If you’re capitalizing something, in accounting terms you’re involved with the balance sheet. So I want to add to my image of two separate worlds these two specific examples from local or complementary currency, LETS and SHARE. Whatever way they’re done, both are needed—not just one of them. And the one on the credit side mustn’t be begun and then run out of steam. It’s the more important one for reasons I’ll explain in a moment.

In accounting terms we also have two worlds: the income and expenditure account and the balance sheet. If one is trying to have an effect on macro developments, it’s crucial to be linked to something that is already completely known to us: namely, accounting. Many people, both alternative and mainstream, don’t grasp the real meaning of accounting, but I want to bring it in as something that is completely concrete and objective; moreover, nobody invented accounting, nor can anybody own it. You cannot have right-wing accounting, nor can you have left-wing accounting. You can argue over whose is the profit, but first you must have a profit in order to say whom it belongs to. A significant aspect of accounting is that it’s almost neutral.

I want to pursue my argument by saying something provocative. Although I am familiar with and more than sympathetic to the complementary currency movement, I also have on a mainstream financial hat. And what I notice among mainstream finance people is a complete lack of interest in local currencies. They smirk at the idea of local currencies because they think the proponents of the idea don’t understand the first thing about monetary matters. In fact, they say that the quicker these people get together and take over the world, the quicker they will find out that they know nothing about monetary policy and the sooner the mistakes in their ideas will become evident.

I understand this attitude. Even in the Social Forum movement, for example, there’s a good deal of earnest and real critique. But the problem remains: How are complementary currencies going to replace the central bank? What are you going to do when you get the levers in your hands that decide whether Zaire does or does not get funded? This is a whole other dimension, and I think it’s necessary to have some sense of what it means. I know there are many problems connected with mainstream finance, but if you are responsible for a country’s finances, you need a level of experience that you simply don’t have if you are only critiquing this task. Therefore, if one wants to make a transition, it’s essential that one be able to assume responsibility for financial issues. In this regard I think the complementary currency movement is an incomplete project. After so many years now, thirty or more, it needs to take a step, if I may say so, into maturity. It needs to come of age a little bit more, and I think it’s quite able to do so. What I mean by this is something that is quite complicated to describe, but I shall try.

Many of our environmental problems, for example, have to do with the power of the corporation today. This is a terribly serious situation, especially in the United States, where normal constraints no longer exist. It is a situation that really must be addressed. Something needs to be done to limit the field of operation, the powers, the rights of the corporation. (For a full treatment of this topic see my book The Right-On Corporation: Transforming the Corporation.) It is essential for the history of humanity because the American approach to corporations is now determining our future. If we could trim tab them—to use Buckminster Fuller’s nautical engineering image of making a small technical adjustment with large-scale effect, such as weighting the rudder of a huge ship to affect its speed or direction—this would have enormous significance, not just for the United States but for the whole world.

Running alongside or behind or underneath this problem of corporate power is something not entirely independent, which plays a role that is invisible and unspoken but determinative, namely, the mantra of ever lower prices and its corollary: lack of income. If this problem is not addressed, the economic changes people are trying to achieve will be almost impossible to bring about. This has to do with the two worlds of money and credit. It shows up as debt for most people, but it can also be insufficient income. In a LETS system, from a macro point of view the main goal should be to engender income between the traders. This means not only paying for local goods but also paying the right price, the price the local baker can afford to live from. It is just as important to trade at a price affordable to the local seller as it is to trade locally. In our buying habits many of us go to our local bakery and put pressure on the baker to match the supermarket price. We say—not directly, perhaps, but by the fact of shopping elsewhere—“If you take a bit off the price, then I won’t go to the local supermarket.” This has to stop because the income the baker needs to live comes from sales. It doesn’t take much insight to see that persistent reduction of price means persistent denial of income. The world over, this is a fundamental economic problem that needs to be addressed.

In the area of money it is essential to make sure that the income we provide—that is, the price we pay for things—is such that the people who are selling can afford to continue to do so. This is an objective step we can take to build an economic life in which people have adequate income. A primary straightforward reason why people go into debt is that they don’t have enough income, but another reason is that by borrowing they get the capital they need but otherwise cannot find. Unfortunately, capital today is not really interested in people’s creativity but rather in maintaining itself, and therefore it seeks security. It’s much easier to get money for your business if you say, “I’ve got a house you can have if I go broke”; it’s very difficult to be capitalized if the collateral is simply the realization of your aim—flying your airplane to where you said you were going to fly it and landing on time. This latter use of capital is linked to creativity, and if creativity were accepted as collateral, it would change the whole world of capital.

Thus, a program like SHARE is more important than the money side of economic life. By and large, the money side is easily understood and managed. In monetary policy, where the aim is to minimize inflation (rising prices), this is done by matching the amount of money in the economy to the available goods. But all monetary policy is made problematical by the working of the financial markets. For those running a domestic monetary policy it’s relatively easy to organize an inflation-free economy if they are dealing only with the needs in their economy, i.e., if there is enough money to buy goods within the United States. The main difficulty here is that investors everywhere, both within and outside the United States, gamble on the U.S. dollar, the value of which affects the whole world economy. And there are always so-called international financial events that distort monetary policy.

Circulation of Capital

Most of us have in the back of our minds that the two worlds—money vs. credit, trade vs. capital—are in fact one. Because we don’t recognize the difference between them, we don’t perceive something that is crucial in modern economic life—perhaps especially in the United States, whose currency operates as the world’s currency—and that is the circulation of capital. You can see what I mean in accounting: normal accounting expects your income to be in excess of your expenditure, and therefore you will have something left over. Your accounts expect your assets to be greater than your liabilities but balanced by your own capital.

In my sketch [see above] each one of the pairs of columns has an upper and lower part of identical length. The lower part is divided into two, with the bottom section on the left indicating surplus and on the right indicating equity. Thus, income less expenditure equals profit; assets less debt equals equity. All accounting expects this; therefore, at the end of the year the profit (or loss) flows to (or from!) the own-capital account on the balance sheet. This is an important image. It’s also crucial to realize that accounts are by and large run annually, and then they are set back to zero. The difference between profit and loss on your activity is then applied to, or taken away from, your balance sheet. For in principle, where there is profitability, there is a flow from operating to balance sheet.

What happens then? If I borrowed money, the flow is initially used to replace what I borrowed. But if we observe any profitable business over time, we’ll see that this has a simple consequence. First, the amount lent is replaced, so what I got from you goes back to you. And then I start stocking money. We call it reserves or retained earnings—call it what you like, but what I do is stock it on my balance sheet. This presents a problem because in economic reality it’s not on my balance sheet. My reserves are out in the world; they’re not in my business. They are trying to flow on.

Many of our problems in modern economic life have to do with the fact that we block or hoard capital, not that we hoard money. It’s much more complicated when we hoard capital; we do not let it flow on. Part of the background for this is that in Western economic life the idea of Jubilee, of writing off capital, is absent except in force majeure or for one’s child. We’re used to saying to our offspring: “Well, it didn’t work out. Never mind.” And then we write off the capital but only because it’s for our own child. It’s much less easy to do for our neighbor’s child. Or if you invest in Argentina and the markets go against you, you say: “Too bad! But I’ll write it off.” It’s not that we don’t write off capital, but we have no active, conscious idea of doing so systematically, of parting with the excess of capital in our world.

The concept of Jubilee comes from the Hebrew culture. Every fifty years or so existing indebtedness would be written off. It’s an extremely important thing to do. If you’ve ever been in debt, to the point where it touches your soul and you can’t sleep at night, you know how much it would mean if the person or entity you owe were to say, “Forget it,” and then were to add, “If you ever have the chance to do the same for someone else, do it.” I don’t mean this as a license to print money and just throw it down the drain, but the fact is that you can really enslave a person through debt. An entrepreneur can become trapped if he or she is capitalized in an indebting way and is then prevented from accomplishing what the financial plan proposed. This is all alchemy, the alchemy of the entrepreneur. The dollars entrepreneurs must borrow for lack of funds prevent them from doing what they are trying to do. My advice is to invest in local enterprise in ways that give wings to the entrepreneur.

In my view, one of our major problems is the jamming up of capital, with its many consequences—the main one being a resulting lack of income. It has to do with our mindset, which leads us to use the world of capital in a certain way; it does not have to do with the structure of the economy or the banking system but with the fact that it’s a real challenge for most of us to say good-bye to our capital. The consequence of our reluctance is huge because in the culture we have we start stocking capital, which has nothing to do with the monetary world. This means we are unaware of that significant phenomenon, namely, the circulation of capital.

It’s essential for us to understand that we need not just to steward capital but to steward the process of the circulation of capital. We must understand that the capital in our world is all that’s needed for what we do, no more and no less, and so it’s important to properly capitalize the local bakery. Don’t half-capitalize it and wish it luck; give it the capital it needs. Conversely, if the local baker starts to become capital rich, he or she shouldn’t retain the excess capital on the balance sheet but should have a sense that it needs to be moved on. In the modern world, especially in the United States, this is done technically but not with the degree of consciousness that could, indeed should, be brought to bear.

A specific example of moving capital can be found in the not-for-profit/for-profit context of the fundraising world. If I make an image of this, here is what happens: A for-profit company, let’s say Coca-Cola (left-hand box in my sketch) wants to be generous, so it identifies a not-for-profit (right-hand box). Both entities have an income/expenditure account and a balance sheet, although the non-profit might not think it does. When Coca-Cola makes a transfer of money to the non-profit, from a tax point of view and from an accounting point of view it can be called a donation, but technically the company is reducing its liability in order to reduce an asset, which means it is transferring an amount of money from cash to cash.

This may be complicated, but it’s absolutely crucial to understand. If I, a for-profit corporation, want to give to you, a not-for-profit corporation, the way I do it in accounting terms is to identify that I have too much on my liability side. I have too much capital, which is a liability, so I determine to reduce it by $1000, and I do this by writing a check against cash. This then appears in the cash account of the recipient, whose own capital is increased by this fact. At this point the recipient board has a decision to make: Does it apply the money received to real estate, for example, or to rehabbing the building? Does the board assign it as income for staff or continue to rely on volunteers?

The main technical problem we face in the monetary world at large is that capital is coagulating, being thought of and stocked as reserves on the capital account, when in fact it has flowed on. We have no sense of the process of circulation, of standing in the river of capital. Awareness of this concept is absent in Western economics, and yet it’s present in the way we do business. Everyone who transfers cash from one’s own business or entity to another has to do it this way: The funds go from the donor’s responsibility to the responsibility of the management of the recipient entity, who must then decide how to apply them.

The real challenge facing the world at large, and therefore facing the complementary currency movement, is to apply far more of donated money as salaries—to pay people with it and not to continue stocking it. If we could understand this point and articulate it in the realm of complementary currencies, there would be macro ramifications throughout the world, albeit locally enacted. We need to have some sense that the world we’re in today, in both economic and financial terms, has the quality of a membrane, which means that we must be careful to avoid “us vs. them” notions. We must avoid harboring the idea that someone else is responsible for our actions or that someone else will sort it all out, whether that someone else be the market or the state. We have to be the first movers in this world, especially in the monetary world, recognizing that if we are, we are freed of external compulsion and in that sense freed of the past. Moreover, because economic life is like a membrane, if only we can think through clearly what we do in our little corner, it will spread all over the world. It cannot be otherwise. There is something about the realm of finance, the monetary realm, that has this logic within it. Whatever we think, will be in the world.

I’ve tried to proceed here today on the level of imagery but also in a way that is completely linked to standard accounting practice. The last thing I want to say is that in the monetary world something is happening which I think needs to be taken on board in the local currency movement. There is in process now the creation of an international set of accounting standards—more technically, a universal set of accounting standards—that is predicated on addressing all the problems I’ve touched on. This means that once these standards are in place, it will matter what they show, how real they are. Will money be fake—that is to say, something unto itself—or proxy, which is what a true money is? What will we be trying to show when we deal with money and capital? I would hope that the complementary currency movement will play a part in the discussion that is taking place on very esoteric levels, so to speak, by resolving the issues on the level of the local bakery. This will not be without effect in the monetary world because, as I say, that world is a membrane. In the monetary world there is no ownership in the normal sense in which we use the word today. Nobody is able to own a membrane.

Thank you for your attention.

Question & Answer Period

(Questions were inaudible; only the answers follow.)

Our culture of cheapness for the sake of cheapness is catastrophic in economic terms. Let’s take the example of the lady who produced today’s lunch. She incurred expenses for the time it took her to prepare, for the ingredients, for the people she employed, and for whatever else she used. If she wants to come out ahead, she has to have an income in excess of what she expended. She may say, “Look, here are the accounts. It cost me $1000 to provide the lunch.” Leaving aside whether she could have saved here or there, let’s assume this is correct in auditing terms. And then the Schumacher Center says, “How about taking 10 percent off if we pay in cash?” Or, “There’s a place that would have done it a little bit cheaper than you did. We may go there next time.”

Or take my case. I used to be in the building trade. I learned never to take on a client who wasn’t going to stay with me. I would never do an estimate for anyone who hadn’t contracted to use me before learning the cost. Otherwise that person would go off to the pub with my estimate and say to a local contractor, “This builder will do the job for ten thousand. Will you do it for nine?”

This sort of thing has to stop because the effect is to make me lose money immediately. It’s a monetary policy issue. There is a glaring contradiction if we say people should have enough money in their pockets to buy the things they need, yet we also keep saying that those things should be cheaper, cheaper, cheaper. This is an impossibility. It’s crucial that the price we pay for everything should be the right price, by which I mean that I can afford to pay you a certain price and you can afford to receive it. Get this right, and the economy will float—not to the level of too high prices, which is the usual expectation, but to a level that is sustainable in strict economic terms.

*

A Local Exchange Trading System is by and large about people trading. Within this system you see the income/expenditure of this person and that person, which incidentally passes through your LETS account. What’s significant about this is the flow of money. It goes on all around the world, and it doesn’t ever end. My income is nothing else but the rest of the world’s expenditure. The fact that I have to close off my accounts at the end of the year for tax purposes doesn’t mean I stop spending or selling. This is a permanent situation we’re all in; we’re buying and selling, meeting one another’s needs, and that causes a permanent flow. It shows up as trade in the world or as income/expenditure in my accounts.

There is another permanent flow in the world that we don’t recognize, and that is the flow of capital. Because of our Western consciousness, because we don’t accept Jubilee notions of forgiving indebtedness, because we are too self-centered, most people in America don’t think of their “own capital” as a liability, yet technically a balance sheet is made up of assets and liabilities. And these must match; they must sum to zero. Liabilities are made up of debt and equity. Equity is a liability in accounting terms, but because we’re so concerned with ourselves, we think equity is an asset. That is nonsense in accounting terms. It simply isn’t. This misapprehension indicates a problem in our mindset that is due to our egotism. If we could overcome our misapprehension, we would see, and accounting will show us, that in the great circulation of capital the amount we need when we step into the river of capital comes through our balance sheet, so we don’t need to hang on to it. We hang on because we forget, or we no longer see, that there is a circulation of capital. We need somehow to understand this, whether it’s through accounting or otherwise so that we undo this block.

*

How can we modify the structure of capitalization so that majority ownership does not decide the future of the company? There is no law that says you shall maximize shareholder benefit in any particular way. It is our mindset that leads us to behave as we do. Convention then assumes it, as does “best practice” on the part of a fund manager, for example.

Look at it over time. As economic life becomes increasingly global, the more we move into a membrane: We are never divorced from the effects of our actions. They come back to us immediately. It won’t be long before the attempt to maximize shareholder benefit by quarter-on-quarter increase will be proven to be the way to minimize shareholder benefit. The more global the economy, the less shareholder benefit can be maximized by putting costs onto someone else’s balance sheet. It won’t work. We need to think in the long term: Where will this lead us? What I am trying to say here is that there’s a huge monetary and financial argument in favor of trim tabbing the corporation so that we don’t use the power of majority ownership to force things in a direction the rest of the world doesn’t want to go in.

*

I’d like to expand on something I said earlier. When you as a not-for-profit receive a donation, it goes into your cash account. Unless its use is specified by the donor, your board then has to decide whether to expend this amount as income or apply it to the capital account. It’s up to you. I know that if you’re strapped for funds or your building is falling down, you might say, “Let’s spend some capital on it.” I say no. Spend it as income, and get enough income so that you can rent your building. I’m against owning buildings. That is such an archaic, old-fashioned, inefficient way of doing things. Rent your building but on terms that allow you to do what you want to do in it. The only problem you will have, apart from thinking this doesn’t leave you free, is that you’ll need to have an income sufficient to pay the rent. I will always argue that even in the not-for-profit world, paying the going rate for people will in the end give a proper value to the organization.

I’m referring specifically to the case of the not-for-profit, but this isn’t about not-for-profit as opposed to for-profit. It’s really just a straight piece of economics in general. In the modern day we need to start paying the going rate for people. We must understand this and then start to move down that path, which will involve our motivational issues and the need to overcome egotism. Shareholders will have to ask: “Do you mean I’ve got to think long term? If you want to recycle water in your hotel, do you mean I’ve got to put up more money and wait even longer?” I would say, “Yes, because if you’re going to insist on short-term returns to capital, you’re the one who will keep me from recycling my water; it’s not me.” I speak from experience with a hotel where this was done. We were lucky to find eight hundred investors over twenty years who said, “We’re investing in you because we’re thinking long term.”

It’s debilitating to have the right ideas but not the capital to realize them, even more so if the mentality behind the capital is still saying, “Now can I have my quarter-on-quarter income increase?” We have to give up certain expectations. The more we can do this, the more capital will become freed up. We are in a membrane, and you can’t do something in one corner of a membrane that won’t happen in another corner.

*

What I’m going to say may not be understood as a piece of economics at first, but it will quickly show up as such. If your organization receives a donation of money and you decide to use it only to pay staff and not to invest it in real estate, two consequences result from this. There will be an alchemical effect on your staff because now they are recognized as human beings and not, with all due respect, as a modern version of slaves; that is to say, they’re either paid for the first time or, if they were being paid, they are now receiving a decent wage, and they know they can put bread on the table and feed their children. Not only will this bring money into the economy, it will bring buoyancy into the souls of human beings. From this, huge resources will unfold.

The other important consequence, perhaps especially in the United States, is that if one doesn’t apply donations to capital one creates the opportunity for somebody else to capitalize what one is doing. In this regard we have now reached a very important stage in economic evolution that may be critical in the United States. It’s one thing to pass donations from Coca Cola to a not-for-profit of its choosing, but it is catastrophic if this is done on the basis of exerting its will over the recipient. Capital should be transferred from one entity to another—systematically, methodically, and without strings. This is something for the recipient to take hold of, and then the donor backs out.

I see the Schumacher Center as an opportunity for many people to give money. This is different from a huge foundation allocating large grants as an extension of its will, with the money to be used specifically for this or that. Entities that have no personal intention but are just doing good works will transfer capital without strings. The foundation world needs to become a little less personal, grants need to be a little less an extension of the grantors’ will and more a means to facilitate the will of the recipients. This too is a trim tab. There’s nothing in the structure of foundations that prevents it, and the whole dynamic in society would change if it happened.

*

Schumacher’s concept of intermediateness, of appropriate scale, is for me sound ground in economic terms. It’s not sensible economics to say only things that are small are beautiful. I think his real argument as an economist was not that. Faced with the huge scale of things, he advocated resizing. His point was that things have to be appropriate to the scale. To give an example, what’s the point for me here in Massachusetts to order Italian spring water? I could as easily order local water. If I want copper for the solenoid of the alternator in my car, however, there’s no way I’m going to get it here in Stockbridge unless I rip it out of your car. Copper is not locally available around the world. We need to recognize the appropriateness of things.

Schumacher may or may not have commented on a problem in modern economics that influences us all whether we’re aware of it or not. It’s described by John Kenneth Galbraith as an unfortunate thought on the part of John Maynard Keynes, who had the idea that there is a macro-economy and a micro-economy. The macro-economy is dealt with by prestigious economists such as Jeffrey Sachs—people “way up there”—and the micro-economy is a matter for you “way down here” in the Berkshires who are trying to figure things out. This is a huge problem in economics because it invites us to think that what we do on the micro level is suddenly subject to different principles when we act on the macro level, whereas economics is really a continuum.

What I do locally—and accounting is the only thing I’ve seen in the world that gives me a sound way of understanding this—should be and needs to be no different from what I would do as the chairman of the Federal Reserve because of it all being a continuum. Instead of saying that in those higher realms a different game is being played, we may ask a Schumacherian question: Where am I on this continuum? What is it appropriate to do whether I’m a local baker or chairman of the Federal Reserve? To the idea of a continuum I would add that no matter whether in high or low office we should all be speaking the same language. If we can understand this and reflect it in our local economies, it will play an enormous role in constructing our modern economic life in a favorable way.

*

If you undertake to capitalize your local business, and you’re really worried about the way the world is going, instruct your broker to liquidate your stock in IBM and buy into the local bakery. But in the process, instruct the broker not to buy A shares but B shares, non-voting stock that gives you no power over the business. Say that you want the right to a return on your capital, but you don’t want the right to tell the baker how to run the business. These are small points in technical terms, but on them turns our motivation. To those who have money in pension funds I would say: “Do yourselves a favor. Buy stock in the local bakery building, and then buy from the baker. Create your own pension fund and the security it brings. Get it out of the markets because, you know, it’s Jubilee time in the pension world.”

This is subtle stuff, but from it can come a whole wellspring of new wealth. To be concrete, when the pension funds collapse, as they are bound to do in a global economy, the fiction that they were secure collapses too. Watch out for when the U.S. dollar starts to falter. Go local in the sense of buying direct stock. Don’t lend money; rather, buy stock in your local bakery in such a way that the owner has the power to do what he or she wants to do with the business. This is a small technical detail, a trim tab, but it’s definitely possible, and this will give a certain strength to what we’re trying to do.

Concluding Remarks

I think today’s lectures pointed to the fact that there’s a great deal already being done—more than we may think—that belongs to the future we all want. If I were to counsel two things, one would be to avoid pointing the finger of blame at others. In a recent article Steve Roach from Morgan Stanley analyzed the problems affecting the American economy; in every single case, he said, it’s an error for Americans to think these problems are caused outside the United States. This is not me being rude to my hosts; this is an American saying that each problem is systematically, technically, methodically caused by the way the people in the United States behave. I’m not trying to make a moral point, but if they want the situation to improve, they will have to modify their behavior. Roach was cautioning against trying to put the blame on the other party. Don’t talk about “them” as the source of the problem. Have the courage to step into the desired world, which in some respects I think is here. Many of the examples given by today’s speakers indicate to me that it is.

Secondly, I would suggest that when the United States began its constitutional journey, there were many ideals that have yet to be fulfilled. On this journey we’ve lost our way. Instead of blaming the environment we find ourselves in, politically and otherwise, we need to backtrack and find a new path.