Monterey Common Cents: Notes on a project in process

This paper represents a dialog that is going on right now between the staff of the Schumacher Center and a citizens group in Monterey, a small town in Western Massachusetts. The thoughts should not be considered to be finished; instead, think of them as part of a process we are undertaking in our effort to find our way toward local prosperity, civility, and environmental harmony.

—Jake Sterling

The Need for an Alternative Currency

Monterey is a community of people who work in small businesses: tradespeople, artisans, artists, store keepers and other small merchants, those who have set up a home office with a computer and an idea, and people who rely on even smaller, cottage industries. It’s a community of self sufficient, independent people who try to support each other in their businesses. Money is hard to come by and what money comes into the town flows out again more easily than it came in.

There is another part of the Monterey community also, the summer people. A sizable part of the local economy is based on the seasonal influx of money that these folks bring. This is money that can be spent outside of Monterey, spent in Monterey and then allowed to flow out of the local economy just as quickly, or it can be spent in Monterey and then re-spent many times over again before it passes out of the community.

Dealing locally is an ideal to which all of us aspire. If we buy from local merchants and hire our neighbors when we have work for them, we help them and strengthen our community. Buying locally produced goods is good for the environment too, reducing energy use and the demand for new roads by eliminating much of the transportation involved in supplying goods over long distances.

We all know these things and yet, whether we are Summer people or permanent residents, the economic forces which encourage and even force us to spend the greater part of our money outside of the local community are very strong.

A group of Monterey citizens has been meeting to address this problem and to try and find if there aren’t ways in which, acting as a community, we can counteract some of those forces, a way to create “positive feedback,” incentives to make it more desirable and even advantageous to deal locally. Working with the staff of the Schumacher Center in Great Barrington, this group has been investigating an alternative currency system that is proving successful in Ithaca, NY, and other cities around the country, with the idea of starting a similar system in Monterey.

Through the use of a locally based currency, or scrip, which might be called “Monterey Common Cents,” we could create a medium of exchange backed by our own goods, services and the good faith of ourselves and our neighbors, which would add to each person’s buying power. Because it would be a local currency usable only in the Monterey area, it would create exactly the kind of incentive to trade locally that is needed.

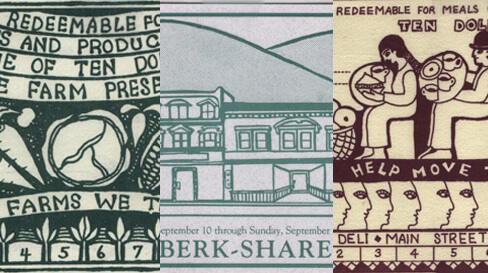

Scrip is just an extension of an idea already familiar to the Monterey community in other local programs like BerkShares, Monterey Store Notes, Deli Dollars, and Berkshire Farm Preserve Notes— programs which have proved so interesting and successful that they have been showcased on Japanese television as well as the four major American networks.

The way it works is quite simple. When you sign up, you are asked what goods you have to sell or what service you will offer for which you are willing to accept partial payment in Common Cents, or, if you work for someone who participates in the Common Cents program, you may want to accept part of your salary in scrip. You can accept any percentage that you like. Your name and what you have to sell are added to a listing that will be published each month in an insert in The Monterey News so that other people can find you, and you are issued an initial three notes—worth approximately one hour of labor, or ten dollars. Just as with U.S. dollars, the actual value of the currency will depend on whatever deal you are able to negotiate. You can use your Common Cents just like regular money at any of the stores or for any of the other goods and services listed in the Common Cents flyer.

Although the goal of the Monterey Common Cents program is increased prosperity and strength in the community, there are some immediate benefits as well. Because goods and services are listed every month, the people who have Common Cents notes will be looking through those listings to find out where to spend them. The scrip will act just like the discount coupons that the supermarket sends to attract business. Unlike discount coupons, however, you can turn right around and spend scrip yourself, or give it out in change to other participants!

Obviously, the more people in the community that take part in the Common Cents program, the more opportunities everyone has to use their scrip. When people realize that there are many opportunities to spend scrip their confidence in it increases. This increased confidence acts to increase the amount people value it.

Ithaca Hours: A Working Scrip System

Here are some things that people in Ithaca, New York have to say about their scrip program, Ithaca HOURS:

Portia provides haircuts, for HOURS and has rented videos. “People really relax and open up when I cut their hair. It’s very interesting to meet people from different walks of life, to share the experiences of different careers. I really like the HOURS concept. When I run out of dollars, I usually have some HOURS.”

Bob’s carpentry offer [in the Ithaca Hours flyer] got him jobs for furniture repair and hauling. “I’ve been laid off lately so I’ve been especially pleased at extra HOUR work.” He’s spent HOURS for his favorite local pottery. “The HOURS are a great idea; all these people are getting needs met that we’d otherwise go without, or pay scarce dollars for. Barter stimulates the local economy. That means I’m stimulated, and who doesn’t like to be stimulated?”

Cathy Draws portraits for HOURS at the Farmer’s Market, and cleans at a local bookstore. “HOURS work out fine; there’s a large variety of ways to use them, they’re just starting to give a boost to portrait sales. I see people who might not have bought if they had to use dollars.”

Chris and Bill have done lots of landscaping for HOURS. They spend them for rent, food and gifts. “HOURS work very well,” says Chris. “We’ve spent lots and are almost out. We’re optimistic about taking even more HOURS this spring.”

Charlie makes drums. “Hours are going great for me. They’ve opened up a lot of things I wouldn’t have been able to afford. They let my wife and I eat out more often, which is good for us as parents—we get more time together and don’t have to deal with cooking. And we were able to afford a potted Christmas tree ‘rather than a cut one, which is better for the environment.”

Allen sells lumber and brings his portable lumber mill to local woodlots. He supplied lumber to Recycle Ithaca’s Bicycles for a wheel rack. “Ithaca Money is a real good idea. It once got me a big job—several weeks of milling wood.”

Alice’s plumbing, carpentry, electrical work, and dog sitting have earned HOURS that have paid rent, bought car repair, restaurant meals and Farmer’s Market food. “HOURS make barter much more possible. I’ve supported myself for over three years entirely on odd jobs, being paid whatever people could afford. Before, when I suggested barter, people were reluctant to incur a personal debt to me; but HOURS are a token of a promise.”

Community-Backed Currency—What does it mean?

We commonly think of money, the dollar bills that we use everyday, as something valuable; but of course they are not; they are just paper. Paper money is really a sophisticated form of l.O.U.. Originally goldsmiths would keep gold in vaults and write out vouchers which could be redeemed by the bearer for the amount of gold indicated on the note. It was of course much more convenient for citizens to handle these notes than it was for them to carry large amounts of heavy gold about. Eventually the governments took over the function of the goldsmiths and legal currencies where developed that were backed up by gold and silver.

Notes such as BerkShares, Monterey Store Notes, Deli Dollars, and Berkshire Farm Preserve Notes are essentially the same sort of l.O.U.. Stores or farms in our area issue notes or coupons stating that they owe the bearer some specific value of goods. Sometimes, as in the case of Deli Dollars or Farm Shares, there is a date set before which the note can not be exchanged. These notes act as a very limited sort of money.

A Common Cents note is essentially an I.O.U. as well. When you receive Common Cents it is worth less than the paper it was printed on. “Legal tinder for all fires, public or private!” But the minute you spend it, you have incurred a debt to the money system. You are promising to redeem that debt by providing goods or services of some kind to anyone else who can pay you in Common Cents. .By incurring that debt you have given the note value to other people.

It is very similar to what happens when you write a check. The check is backed by the money in your bank account. The bearer of the check can carry it around for a short or a long time, or he or she can sign it over to someone else. Eventually, though, that check gets back to your bank and the money is paid out of your account. A check is essentially an I.O.U. also.

With scrip, however, things are a little less straightforward than they are with checks. No one is going to come to you and demand that you turn over goods or that you work at whatever that person might want you to do. What you have promised is that you in your rum will accept scrip as money in payment for some of the goods or services that you have to sell. This may mean that you make something, sell something or have a service that you perform in exchange for scrip, that you accept part of your salary in scrip, or even simply that you are willing to receive scrip as change in local stores.

When you initiate new scrip into circulation, you are essentially borrowing money, though, in fact you may receive some scrip free when you sign up. (This is discussed more thoroughly below.) If find at some point that you are holding more scrip than you have initiated, you can say that the system is in debt to you. At any given time you can calculate your status simply by comparing the amount of scrip that you have initiated to the amount you hold at the moment. For instance, if you started with four Common Cents units (the denominations have not been decided upon yet) and now you hold six, then the system “owes” you the value of two units in goods or services. If you only hold two units, then you still have two outstanding and you “owe” the system their value in goods and services.

You will notice that in this sort of accounting it is always the goods and services and not the currency that is considered to be valuable. This understanding is very important because it constantly returns us to concrete thinking about money as opposed to the often disastrous abstract thinking that occurs when we attribute the value of money to the paper money itself.

Money must be backed by something in order for it to be worth anything. In the old system it was backed by gold. U.S. dollars are backed by the credibility of the Federal Reserve banking system. The community, made up of individuals, will be the backer of Monterey Common Cents. Each individual makes a small commitment, incurs a small debt and gives his or her word on it. So the currency is in a very real sense as good as the word of the individuals who back it. But the weight of this debt is not on any one person’s shoulders: it is a community commitment, and just like with any currency, it can work because the participants generally respect and cooperate with the system. In return, the system helps to improve the community members’ prosperity and the variety of goods and services available to them.

No Interest!?!

One of the ways that a scrip system can help a local economy prosper is by making credit available virtually without interest. When you borrow money from another person, you are borrowing money that already exists and which he or she might profitably use in some other way if you weren’t using it. In our society (though this is not true in all cultures) we generally consider it reasonable to charge a use fee. We call this fee “interest.”

When you borrow Common Cents, on the other hand, you are not borrowing it from another person nor are you borrowing it from an institution. You are not preventing the owner of the money from using it for any other purpose because the money you are borrowing doesn’t even exist before you borrow it. There can, therefore, be no question of a “use fee.” No interest.

Of course there are administration expenses that must be met, but these are minor and can be covered by in several different ways. In Ithaca these costs are met through charging for advertising in the flyer that has the listings of all the goods and services that are available for Ithaca Hours.

Some Problems To Do with How Scrip is Issued

One of the problems that some alternative currency systems such as LETS (a computer based “information” system of exchange) have had is that it is easy for an individual to build up a large debt to the community monetary system and then find that they have no way to repay it.

Another, subtler problem occurs when a member doesn’t put his or her scrip back into circulation either because she is hoarding it or because he is unable to find ways to spend it. This is bad for the person who is holding scrip because he or she is not getting the value that is possible from his or her money. It is also bad for the community, because it reduces the amount of money in circulation and therefore the amount of economic activity that can go on.

The most difficult part of an alternative money system is finding ways to make money readily available to those who need it while at the same time ensuring that people are .neither running up debts that they can’t repay, nor building up stores of “dead” money. The way in which scrip is issued can either relieve or exacerbate these problems. There are essentially three ways that scrip can enter into circulation: it can be loaned, it can be earned in return for service to the community, and it can be given away. It should be understood that in the last two cases where it appears that scrip is simply being printed and used, that there is still a debt involved, it is just ignored. In other words, the community goes into debt to itself but defaults on the loan. This is possible in a limited way because the benefit of getting money into circulation outweighs the loss. However, if this practice is carried too far, the currency becomes over-inflated, people lose confidence in it, and it becomes worthless.

Most often, Scrip is given away in the early days of a project. In Ithaca it has worked this way: you sign up and commit yourself to accepting HOURS in some part of your economic activity, you pay a few dollars to cover administrative costs and youf are issued four Ithaca HOURS, worth approximately $40.

A community may choose to pay scrip in exchange for community service. Since one of the main purposes of an alternative currency is to solve the problem of underemployment, this is an elegant method of issuing currency as it targets people who are want to work but are having difficulty finding jobs. The problem of debt remains, however, and must either be absorbed by the whole community as a sort of invisible tax, or some other solution must be found. From the Isle of Guernsey, off the coast of Britain, comes a delightful story about how new markets and roads were financed by issuing scrip. The debt was repaid with user fees, but since there was no interest involved the total cost was much lower than it would otherwise have been. (The Isle of Guernsey has been issuing its own Currency for more than 100 years.)

In practice, it seems that the best idea may be to use a combination of methods. It is important, when starting an alternative currency, to get a good supply of money circulating quickly so that people have something to spend. This method of getting the money flowing must eventually give way to a more stringent accounting in order to avoid people just taking advantage of the scrip system.

Reading List

If you want to learn more about alternative the benefits of alternative currencies you may be interested in the these books from our publications list:

Interest and Inflation Free Money by Margarit Kennedy

Inflation and the Coming Keynesian Crisis by Ralph Borsodi

The Need for Local Currency by Robert Swann

Cities and the Wealth of Nations by Jane Jacobs

The Vermont Papers by John McClaughry

Building Sustainable Communities by Swann, Benello, & Turnbull.

The library at the Schumacher Center, just outside of Great Barrington, Massachusetts, is a resource for further study. The Library is dedicated to regional and decentralist economics and land issues. You can contact the Schumacher Center for further assistance.